Local Tenant Protections Stir Economic Concerns in California Housing Policy

November 5, 2025

New York Proposes AI Oversight for Professional Fields

November 10, 2025

November 7, 2025

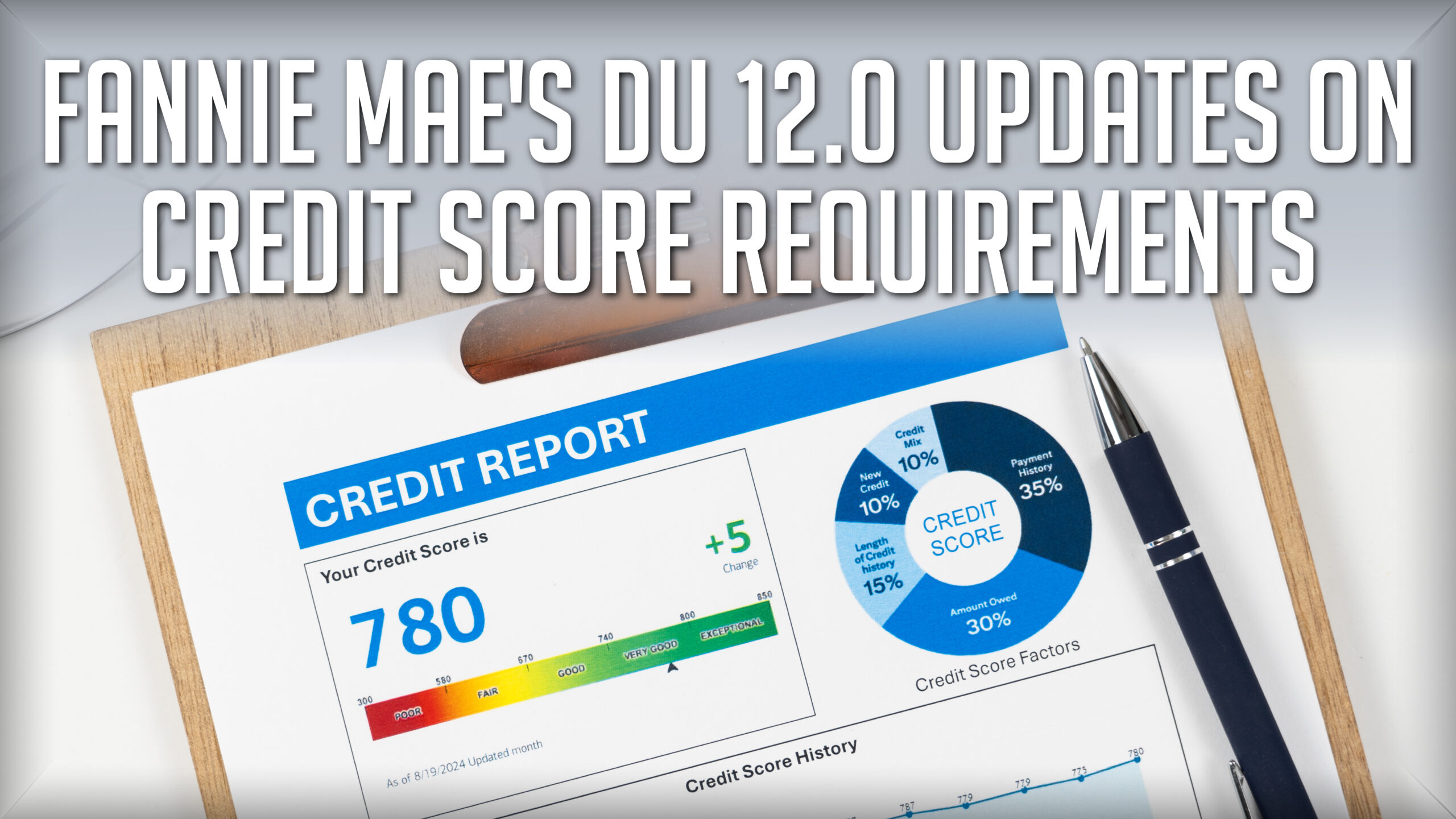

Fannie Mae will implement a significant Desktop Underwriter (“DU”) update during the weekend of November 15, 2025. For new loan casefiles on or after November 16, 2025, there will no longer be the minimum representative and average median credit score requirements of 620. Instead of a fixed numeric threshold, DU Version 12.0 will rely on an internal credit risk assessment drawn from borrower and loan characteristics to determine eligibility. This DU update by Fannie Mae may indicate a shift toward risk-based evaluation rather than score-based gating which may better align Fannie Mae’s underwriting process with its broader credit-risk management framework.

DU 12.0 will also remove the 720-score requirement for borrowers financing second homes or investment properties with seven (7) to ten (10) financed properties. These changes apply to all new or resubmitted DU loan casefiles created on or after the weekend of November 15, 2025.

Lenders are reminded that they are still responsible for ensuring that credit scores for all borrowers are requested from the permitted credit score versions outlined in “Section B3-5.1-01, General Requirements for Credit Scores” set forth in the Selling Guide. We will keep our readers informed on key details as Fannie Mae continues to modernize its automated underwriting model to expand access and align further with the Selling Guide.

For the full text of the DU Version 12.0 November Update click HERE.

DISCLAIMER

This publication may constitute attorney advertising under the laws and rules of professional conduct of one or more states. The information provided in this publication is for general informational purposes only and does not constitute legal advice. The contents are not intended to be a substitute for professional legal advice, consultation, or representation. No attorney-client relationship is formed by reading or relying on this publication. Prior results do not guarantee a similar outcome. Readers should consult a qualified attorney for advice regarding their individual circumstances or any specific legal questions they may have.

If you have questions about this publication, please contact Adam Friedman, Ralph Vartolo or Michael DeRosa,

Friedman Vartolo LLP, 1325 Franklin Avenue, Suite 160, Garden City, NY 11530, Phone: (212) 471-5100 | Fax: (212) 471-5150.

{kind=link}

{kind=link}

{kind=link}